Content

- Earnings:

- Let us understand how to account for derivatives!

- Accumulated other comprehensive income

- IASB announces membership of the transition resource group for IFRS 17

- Global IFRS Insurance Survey 2018 — 2021 countdown underway: Insurers prepare for IFRS 17 implementation

- IMPACT ON LDTI – TRADITIONAL PRODUCTS

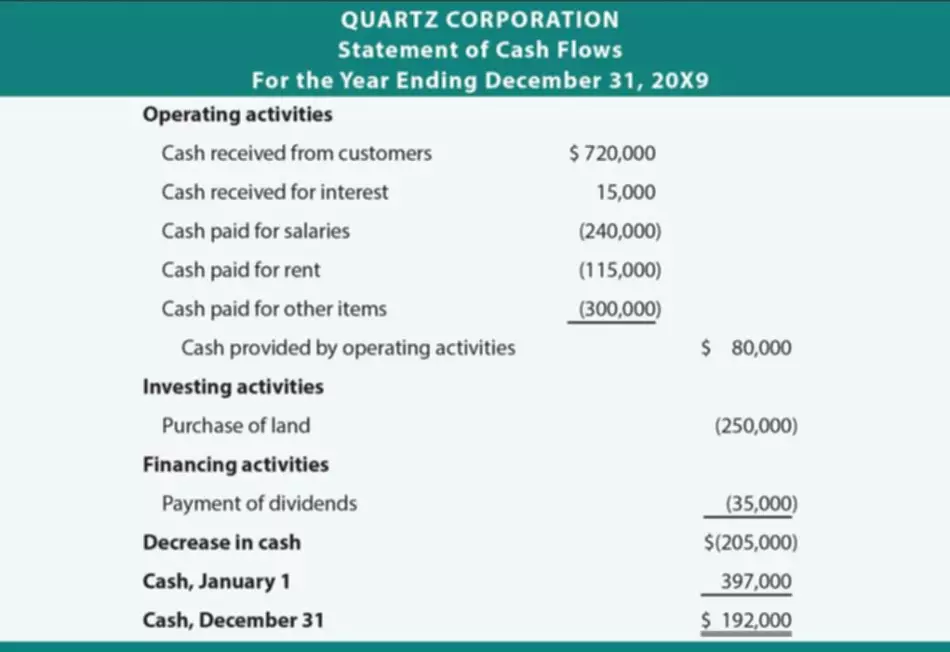

- How Should the Restructuring Gain Be Reported on Income Statements?

Combining net income and OCI in one statement enhances the prominence of OCI but may diminish the importance of net income. It may also confuse investors because net income tends to be buried within comprehensive income and becomes a subtotal in the middle of a continuous statement of comprehensive income. This dilutes the focus on net income as the most important performance measure of a company and draws the attention of the financial statement users away from net income to OCI as the “bottom line” of a business. The close proximity of the components of changes in OCI and earnings per share also may further confuse investors. And placing OCI between net income and earnings per share may be misleading to investors. Similarly, there is no stranded effect when a deferred tax asset and valuation allowance for the same amount were originally recognized through OCI, but subsequently the valuation allowance was released through income tax expense. This is because the income tax rate differential impact on the gross deferred tax asset is offset by an equal impact on the gross valuation allowance in OCI.

What type of account is AOCI?

Accumulated other comprehensive income is a general ledger account that is classified within the equity section of the balance sheet. It is used to accumulate unrealized gains and unrealized losses on those line items in the income statement that are classified within the other comprehensive income category.

The discussion here was limited and a continuation of some of the items highlighted in the opening debate around what should be reported in OCI. Some believed the rate at inception was not the appropriate rate, but most generally felt this was the only acceptable solution. The intent is to hold the investment and to collect interest and principal until maturity, so the classification should be amortized cost. The impairment losses can be reversed if the investment values increase. Verex follows IFRS because only IFRS companies can account for investments using the FVOCI classification. In this case, the FVOCI is without recycling because these are equities. The FASB received 72 comment letters in response to the May 2010 proposed ASU exposure draft.

Earnings:

This format further allows financial statement users and management to focus on and discuss the current performance as summarized in net income and the OCI in order to assess a company’s actual liquidity and future cash flow requirements. The components of other comprehensive income present valuable information about a company’s potential future net income and cash flows from transactions generally to be finalized sometime in the future. If the intent to sell does not exist, the entity must next determine whether it is more likely than not that it will be required to sell the impaired debt security before recovery of its amortized cost basis.

Pulling up that picture from above again, we see that a large component of the Statement of Comprehensive Income is Foreign currency translation adjustment. When these two metrics vary widely, we have a situation where Net Income probably isn’t accurately recording the actual growth reality of a business, making metrics such as P/E mostly useless. Note how the company chose to put Unrealized Gains and Losses inside their AOCI calculation, and then adjusted it out of OCI (subtracted $134 as a reclassification away OCI towards Net Income). It defines where those new Unrealized Gains and Losses contribute to the Income Statement, leaving a potential gray area. We now have a situation that used to be defined inside OCI and instead flows through the Income Statement, which could unlock lots of opportunities of hidden value for those investors who are paying attention. Once we found AOCI in the Retained Earnings part of the Balance Sheet, we can also see how OCI’s annual figure plays into that.

Let us understand how to account for derivatives!

If, for example, the stock was purchased at $20 per share, and the fair market value is now $35 per share, the unrealized gain is $15 per share. The idea of OCI is that it will present certain gains and losses that have been recognised directly in equity during the year because accounting standards prohibit their recognition aoci vs oci in the profit and loss account. An example of such a gain not included in the profit and loss account and thus appearing in OCI is a simple revaluation on property, plant and equipment. Other examples include group foreign exchange differences and remeasurement gains or losses on defined benefit pension schemes.

Displaying the components of other comprehensive income below the net income total in an income statement reporting results of operations (the one-statement approach). When a full or partial valuation allowance was previously maintained, or is maintained as of the enactment date, it is essential to determine what portion was or is currently recognized or adjusted through OCI versus income tax expense.

Accumulated other comprehensive income

Non-financial companies that hold large amounts of equity securities – mostly tech giants such as Apple , Alphabet , and Microsoft – include all gains and losses on those securities as part of “Other income ”. For investments that are not consolidated into a company’s financials or accounted for under the equity method, there are now only two options for companies. The can either recognize changes in fair value directly through net income, or they can use a method of accounting similar to the cost method described above. Under IFRS, for example, gains on revaluations of property, plant, and equipment are recognized in OCI while gains and losses on remeasurement of investment properties are recognized in profit or loss. GAAP with respect to whether amounts initially recognized in OCI are reclassified later to profit or loss. Under U.S. GAAP, such items are eventually reclassified into profit or loss, whereas, under IFRS, different items are reclassified in different ways (e.g., actuarial gains and losses related to employee benefit plans recognized initially in OCI aren’t reclassified into profit or loss). All entities must disclose their accounting policy for releasing stranded tax effects from AOCI, i.e., either to retained earnings or income tax expense .

- However, it is the best option I have for companies that don’t provide full disclosure of their cumulative unrealized gains/losses.

- It is commonly referred to as “OCI” although the word comprehensive has no meaning as can be seen from the definitory equation.

- The results from discontinued operations and gains or losses from extraordinary items — such as a fire or a flood — are also part of net income.

- Basu holds a Bachelor of Engineering from Memorial University of Newfoundland, a Master of Business Administration from the University of Ottawa and holds the Canadian Investment Manager designation from the Canadian Securities Institute.

- In business accounting, other comprehensive income includes revenues, expenses, gains, and losses that have yet to be realized.

To me when we talk about OCI; we refer to those changes resulting from other, non-primary or non-revenue producing activities of the company that are not reported in profit or loss as required by a specific IFRS standard. Due to the fact that the main equity elements are Share capital, or Retained Earnings may be. The others can be aggregated to OCE and this can cover elements like Share premiums, Revaluation https://simple-accounting.org/ reserves, NCI, General reserves, Translation reserves etc. Over the past year, interest-rate volatility has increased because of, among other factors, the impact of monetary policy. An unrealized gain or loss means that no sell transaction has occurred. Other comprehensive income reports unrealized gains and losses for certain investments based on the fair value of the security as of the balance sheet date.

Financial statements are written records that convey the business activities and the financial performance of a company. The impacts are spread throughout the balance sheet, from Goodwill adjustments to Retirement obligations to the value of Cash and Cash Equivalents. It explains why Shareholder’s Equity didn’t increase related to traditional Retained Earnings. However, what’s not clear until we examined OCI is that discussion of the results of operations doesn’t fully disclose the impacts of currency for this business. The IASB majority of 10 vs. 2 supported the staff recommendation to reject an asset recognition basis for ACs. The staff recommendation was split again with the FASB staff recommending a loss recognition test whilst the IASB staff did not recommend a loss recognition test.

The most significant discussion was around the second issue and what amount should be presented in OCI. Others believed the proposal, although not perfect, was better than current accounting and was necessary in light of previous decisions made on accounting for the assets and fulfilment value liabilities. In either view, the discussions seemed to solidify consensus in the need for an OCI solution to be included as a continuous statement within the statement of comprehensive income and to be discussed separately. After that point, I collect the incremental unrealized gains/losses in each reporting period.

Global IFRS Insurance Survey 2018 — 2021 countdown underway: Insurers prepare for IFRS 17 implementation

The loss is measured as the difference between the carrying amount and higher of the present value of the revised expected cash flows, dis- counted at the current market discount rate and the estimated net realizable value of the investment. Investors need to make these adjustments, both to the NOPAT and invested capital, in order to accurately understand the cash flows of companies impacted by the new rule and ensure the greatest degree of comparability with historical results. New Constructs, LLCIn terms of understanding the invested capital of the business, the cost basis is clearly the number one should care about, as it’s the actual capital Berkshire invested, and upon which it must earn a return. Berkshire was forced to recognize $22.7 billion in losses (9% of revenue) on investments it plans to hold for the long term simply because the market was down in 2018. Investors that rely on GAAP net income would think that Berkshire’s profits declined from $44.9 billion in 2017 to $4 billion in 2018, a 90% decrease. My adjustments, including an adjustment for unrealized losses, show that NOPAT actually increased by 15% over that same time.

Hydro One : CONDENSED INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (unaudited) For the three and nine months ended September 30, 2022 and 2021 – Form 6-K – Marketscreener.com

Hydro One : CONDENSED INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (unaudited) For the three and nine months ended September 30, 2022 and 2021 – Form 6-K.

Posted: Mon, 14 Nov 2022 12:24:26 GMT [source]